The Invisible Tax: How Value Added Tax Shapes Prices, Business Cash Flow and Consumer Spending

Value Added Tax is one of the most common taxes in modern economies, yet many people only notice it when a receipt looks higher than expected.

It appears at the supermarket. It appears on professional invoices. It appears in imported goods. It appears in software subscriptions, construction materials, fuel-related costs, business supplies, household purchases and service contracts. For consumers, VAT often feels like part of the price. For business owners, it can become a monthly compliance obligation, a cash-flow challenge and a pricing decision. For governments, it is a major source of revenue because it is collected through the normal flow of trade.

VAT is powerful because it hides in plain sight.

Unlike income tax, which is often associated with salaries, profits or annual filings, VAT is tied to consumption. It is charged when taxable goods or services are supplied. A business may collect VAT from customers, deduct VAT paid on qualifying business purchases, and remit the difference to the tax authority. The tax moves through the supply chain, but the final economic burden usually rests with the end consumer.

The Organisation for Economic Co-operation and Development describes VAT as a tax on final consumption, levied on value added at each stage of production and distribution, then ultimately passed to the end consumer. :contentReference[oaicite:2]{index=2}

This structure makes VAT different from a simple retail sales tax. VAT is not collected only at the final sale. It is collected in stages. Each VAT-registered business accounts for the tax on the value it adds. This is why the system can be efficient for governments but demanding for businesses. Every registered business becomes part collector, part recordkeeper and part compliance agent.

Understanding VAT is therefore not only a tax issue. It is a financial literacy issue. It affects household purchasing power, small business pricing, invoice design, cash-flow planning, bookkeeping discipline, import costs, supplier selection and profit margins.

A person who does not understand VAT may confuse tax collected with business income. A business owner who does not understand VAT may underprice services, spend money that belongs to the tax authority, fail to claim allowable input tax or miss filing deadlines. A consumer who does not understand VAT may underestimate how taxes shape the final cost of living.

VAT is not merely a line on an invoice. It is a financial system woven into everyday commerce.

What Value Added Tax Really Means

Value Added Tax is an indirect tax charged on taxable goods and services. It is called indirect because the person who ultimately bears the cost is not usually the person who remits the tax to the government. Consumers pay VAT through prices. Registered businesses collect it and account for it.

In Kenya, the Kenya Revenue Authority explains VAT as an indirect tax paid by the person who consumes taxable goods and taxable services supplied in Kenya or imported into Kenya. KRA also states that VAT on local supplies is collected at designated points by VAT-registered persons acting as agents of government, while VAT on imported goods and services is paid by the importer. :contentReference[oaicite:3]{index=3}

The phrase “value added” is important. At each stage of production or distribution, a business adds something: raw materials become manufactured goods, goods are transported, packaged, distributed, marketed, wholesaled, retailed or transformed into a service. VAT is designed to tax the value added at each stage rather than tax the full value repeatedly without credit.

This is why VAT systems use input tax and output tax.

Output tax is the VAT a registered business charges customers on taxable sales. Input tax is the VAT the business pays on qualifying purchases used to make taxable supplies. The business usually remits the difference between output tax and allowable input tax. KRA explains the formula as output tax minus input tax equals tax payable. :contentReference[oaicite:4]{index=4}

For a business owner, this distinction is essential. VAT collected from customers is not revenue in the ordinary sense. It is money collected on behalf of the tax authority. VAT paid to suppliers may be recoverable if it meets the legal requirements. The business is responsible for tracking both correctly.

A Simple VAT Example

Imagine a furniture maker buys timber for a net price of KES 10,000. If VAT is charged at 16 percent, the supplier adds KES 1,600 VAT, making the gross purchase price KES 11,600. The furniture maker has paid KES 1,600 in input tax.

The furniture maker then turns the timber into a table and sells it for a net price of KES 18,000. At 16 percent VAT, the customer is charged KES 2,880 VAT, making the gross selling price KES 20,880. The KES 2,880 is output tax.

The furniture maker does not simply keep the KES 2,880. If the input tax of KES 1,600 is deductible, the VAT payable is KES 2,880 minus KES 1,600, which equals KES 1,280.

The tax authority receives VAT on the value added by the furniture maker. The consumer pays VAT as part of the final price. The business accounts for the difference.

This example explains why VAT is not supposed to tax the same value repeatedly at every stage without relief. The input tax credit mechanism prevents cascading tax where tax is charged on tax at each stage. But this only works when businesses keep proper records, hold valid tax invoices and file correctly.

Why Consumers Usually Bear the Cost

Although businesses collect and remit VAT, the final consumer usually bears the economic cost. This is because a consumer at the end of the chain does not normally recover VAT. The consumer buys the final good or service and pays the VAT-inclusive price.

A VAT-registered business buying goods for taxable business activity may claim allowable input tax. A consumer buying groceries, furniture, electronics or services for personal use cannot usually recover VAT. This makes VAT a consumption tax.

This also explains why VAT can feel invisible. Consumers may not calculate it separately. They simply see the final shelf price, invoice total or receipt. In some cases, prices are displayed VAT-inclusive. In other cases, especially business-to-business transactions, prices may be quoted before VAT and then VAT is added on the invoice.

For households, VAT affects purchasing power. A higher VAT rate or wider tax base can raise the price of many goods and services. A lower rate, zero-rating or exemption can reduce tax included in certain items, though the final consumer benefit depends on pricing behavior, supply chains and competition.

For policymakers, VAT is attractive because it can raise revenue broadly. For consumers, especially lower-income households, VAT can be sensitive because a larger share of income may be spent on consumption. This is why many VAT systems use exemptions, zero-rates or reduced rates for selected essential goods and services.

VAT Rates, Zero-Rating and Exempt Supplies

VAT systems usually classify supplies into categories. The exact categories differ by country, but the most common are standard-rated supplies, zero-rated supplies and exempt supplies.

Standard-rated supplies are taxable at the general VAT rate. In Kenya, KRA lists the general VAT rate as 16 percent for taxable goods and services other than zero-rated supplies. It also lists a 0 percent rate for specific supplies in the Second Schedule to the VAT Act, 2013. :contentReference[oaicite:5]{index=5}

Zero-rated supplies are taxable supplies charged at 0 percent. This may sound similar to exemption, but it is different. A business making zero-rated supplies may still be able to claim input tax related to those taxable supplies, depending on the law. Zero-rating can therefore remove VAT from the final price while preserving input tax recovery.

Exempt supplies are not taxable supplies. KRA notes that exempt supplies are not taxable and related input tax is not deductible; taxpayers who only make exempt supplies are not required to register for VAT. :contentReference[oaicite:6]{index=6}

This distinction can have major business consequences. A business selling exempt services may not charge VAT, but it may also be unable to recover VAT paid on related expenses. That unrecovered VAT becomes a cost. A business selling zero-rated goods may charge 0 percent VAT but still have input tax recovery rights. A business selling standard-rated goods charges VAT and claims allowable input tax.

Many business owners misunderstand this difference. They assume “no VAT charged” always means the same thing. It does not. Zero-rated and exempt supplies can produce very different financial outcomes.

VAT Registration: When a Business Enters the System

VAT registration turns a business into a formal participant in the VAT system. Once registered, the business must charge VAT on taxable supplies, issue compliant tax invoices, file returns, keep records and remit tax due.

In Kenya, KRA states that any person supplying or expecting to supply taxable goods and taxable services worth KES 5 million or more in a year is required to register for VAT. KRA also notes that voluntary registration may be granted below that threshold subject to conditions. :contentReference[oaicite:7]{index=7}

The registration threshold matters because it protects very small businesses from the administrative burden of VAT while bringing larger businesses into the tax net. But a business approaching the threshold must plan ahead. Waiting until after crossing the line can create compliance problems, pricing confusion and unexpected liabilities.

Voluntary registration can sometimes be useful. A business selling mainly to VAT-registered customers may want to register so customers can claim input tax. A business with significant VAT-bearing costs may prefer to recover input tax where allowed. A business seeking to appear formal to corporate clients may find registration helpful.

But voluntary registration also creates obligations. The business must file returns, maintain records, comply with invoicing rules and manage VAT cash flow. A small business should not register casually without understanding the administrative burden.

VAT and Pricing: The Mistake That Destroys Margins

One of the most expensive VAT mistakes is pricing incorrectly.

A business owner may quote a customer KES 100,000 for a service, thinking this is the amount the business will keep. If the business is VAT-registered and the price is treated as VAT-inclusive, the actual revenue before VAT is lower. At a 16 percent VAT rate, a VAT-inclusive price of KES 100,000 contains VAT of approximately KES 13,793. The net revenue is approximately KES 86,207.

If the owner intended to earn KES 100,000 before VAT, the invoice should have been KES 100,000 plus VAT, making the total KES 116,000.

This difference can destroy margins. A business may think it has priced profitably but later discover that part of the quoted price belongs to the tax authority. The problem is especially common among freelancers, consultants, contractors and small businesses that become VAT-registered after years of quoting simple all-inclusive prices.

Every VAT-registered business must decide how it quotes prices. Business-to-business clients often expect prices to be shown before VAT, with VAT added separately. Retail consumers may expect VAT-inclusive pricing. The key is clarity. Quotations, contracts and invoices should state whether prices are inclusive or exclusive of VAT.

VAT is not an afterthought. It is part of pricing strategy.

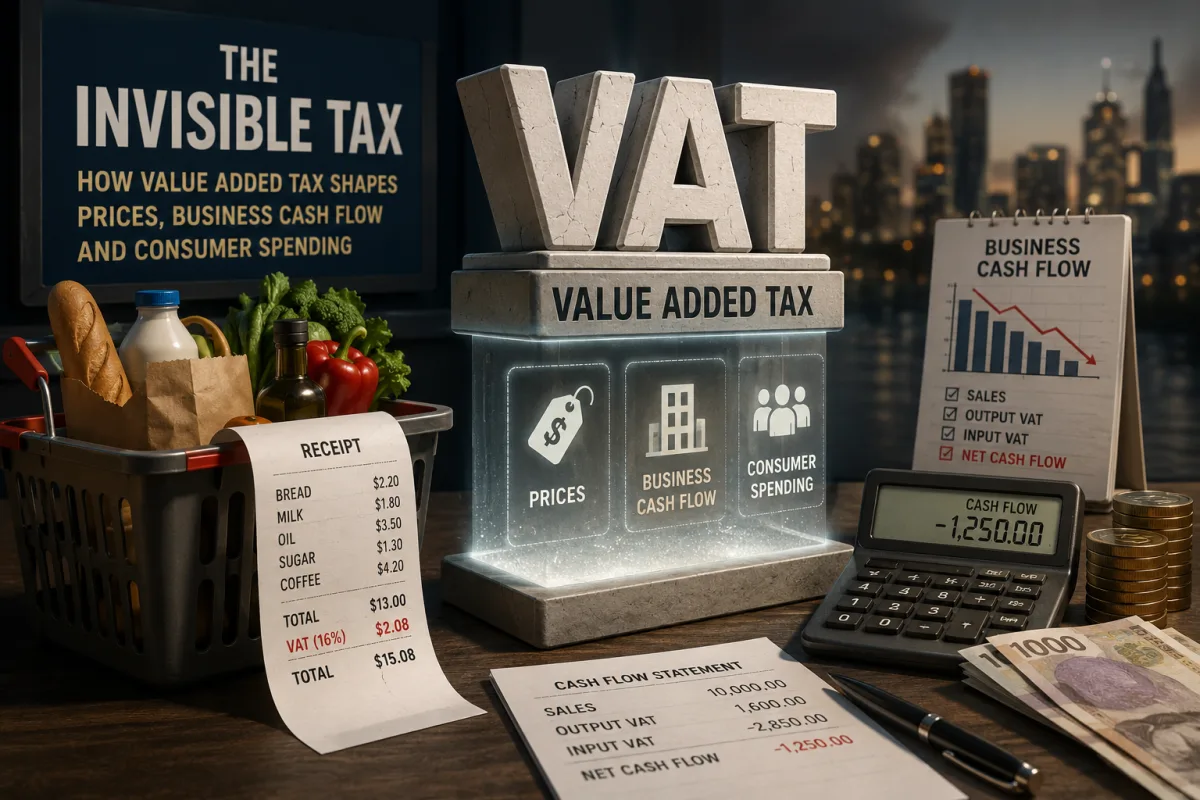

VAT and Cash Flow

VAT can create a serious cash-flow problem when businesses collect late but must account for tax earlier.

If a business issues an invoice and VAT becomes due before the customer pays, the business may need to remit VAT using its own cash. This is especially difficult for contractors, consultants and suppliers dealing with slow-paying clients. The business has not yet received the money, but the tax obligation may already exist.

In Kenya, KRA explains that the tax point is the earliest of several events, including delivery of goods or performance of services, issuance of an invoice, receipt of payment, and certain certification events for supervised work. :contentReference[oaicite:8]{index=8}

This means timing matters. Businesses must understand when VAT becomes due, not merely when cash is received. Poor timing can create liquidity pressure. A business may be profitable on paper but short of cash because VAT, payroll, suppliers and operating expenses are due before customers settle invoices.

Good VAT cash-flow management includes prompt invoicing, clear payment terms, follow-up discipline, tax reserves, customer credit checks and avoiding the use of VAT collected as working capital. The VAT portion of customer receipts should be mentally separated from business income. Spending it creates a future tax problem.

Input Tax: The VAT Businesses Can Often Recover

Input tax is VAT paid by a registered business on purchases used to make taxable supplies. Claiming input tax reduces the VAT payable. But input tax recovery is not automatic. It usually requires that the purchase relates to taxable business activity and that the business holds valid supporting documents.

KRA states that input tax deductions can only be made for supplies or imports acquired to make taxable supplies and that the registered person must possess valid documentation. KRA also states that input tax deduction is valid for only six months after the end of the tax period in which the supply or importation occurred. :contentReference[oaicite:9]{index=9}

This makes bookkeeping discipline valuable. A business that loses invoices, delays bookkeeping or fails to capture purchases may lose input tax claims. The cost is real. Every missed valid input tax claim increases the VAT payable or reduces available credits.

Businesses should maintain organized records for purchases, imports, expenses, credit notes, debit notes, sales invoices, payment evidence and tax returns. Digital systems can help, but the process must be consistent. VAT compliance is much harder when records are reconstructed at the last minute.

Input tax is not a bonus. It is part of the VAT mechanism. Businesses that manage it well protect cash flow and margins.

Output Tax: The VAT Charged to Customers

Output tax is VAT charged on taxable sales. A VAT-registered business must account for output tax whether it sells goods, provides services or imports taxable goods and services into the relevant tax system.

Output tax should be calculated correctly, invoiced correctly and reported correctly. Errors can arise when a business applies the wrong rate, treats taxable supplies as exempt, fails to charge VAT after registration, issues non-compliant invoices or records sales inconsistently.

Output tax mistakes can be costly because the tax authority may still demand the VAT even if the business failed to collect it from the customer. If a business should have charged VAT but did not, it may have to pay VAT from its own funds. Recovering the amount from customers later can be difficult, especially if contracts did not address VAT clearly.

This is why VAT should be built into contracts, proposals and invoicing systems. A business should know whether its supplies are taxable, exempt or zero-rated before quoting. It should know whether the customer is local, foreign, registered, exempt or withholding VAT where applicable. It should know whether imported services rules apply.

Output tax is not simply a calculation. It is a compliance responsibility.

Tax Invoices and Documentation

VAT systems depend heavily on documentation. A tax invoice is the evidence that a taxable supply occurred and that VAT was charged. It supports the seller’s output tax and the buyer’s input tax claim.

KRA explains that a tax invoice is issued by a registered person and contains details of the sale transaction, including VAT charged. KRA also states that a tax invoice should be serially numbered and generated from eTIMS, and that electronic tax invoices in Kenya are generated from compliant Electronic Tax Register systems or eTIMS. :contentReference[oaicite:10]{index=10}

For businesses, invoice discipline is not optional. A missing or invalid invoice can prevent input tax recovery. Incorrect invoice details can create disputes. Duplicate invoices, incorrect PINs, wrong VAT amounts or delayed credit notes can complicate returns.

For customers, especially VAT-registered business customers, a valid tax invoice matters because it supports input tax deduction. This is why corporate clients may refuse to process payments without proper tax documentation.

Good tax invoicing protects both sides of the transaction.

VAT Filing and Payment Deadlines

VAT is usually filed periodically. The filing cycle depends on the jurisdiction. In Kenya, KRA states that VAT returns and payment are due on or before the 20th day of the following month, with returns submitted online through iTax. :contentReference[oaicite:11]{index=11}

Deadlines matter because VAT is not a once-a-year issue for registered businesses. It is a recurring obligation. Missing returns can lead to penalties, interest, compliance restrictions, reputational problems and difficulty obtaining tax compliance documents.

A business should therefore treat VAT filing as part of its monthly financial rhythm. Sales should be reconciled. Purchases should be reviewed. Input tax should be supported. Output tax should be checked. Returns should be filed before the deadline, not at the last moment.

Many small businesses struggle because they treat tax as an event rather than a system. VAT compliance is easier when bookkeeping happens throughout the month. Waiting until the deadline creates errors, stress and missed claims.

VAT on Imported Goods and Services

VAT does not apply only to local sales. Imported goods and services can also attract VAT.

When goods are imported, VAT may be paid at importation based on customs valuation and applicable rules. This affects landed cost. A business importing inventory must include import VAT, customs duty, freight, clearing charges, port charges and other costs when calculating selling prices and margins.

Imported services can also create VAT obligations. KRA explains that VAT on imported services may be referred to as reverse VAT, and that any importer of an imported service is liable to pay VAT on the imported service irrespective of VAT registration status. KRA also states that VAT on imported services is due at the earliest of receiving the taxable service, receiving an invoice, or making payment. :contentReference[oaicite:12]{index=12}

This is especially important in a digital economy. Businesses buy software subscriptions, online advertising, cloud services, consulting, design, licensing, technical support and other services from non-resident suppliers. These purchases may create VAT obligations even when the foreign supplier does not charge local VAT.

Business owners should not assume that buying from abroad avoids VAT. Cross-border services often require careful tax review.

Digital Marketplace Supplies

Digital commerce has made VAT systems more complex. Services can be supplied across borders without a physical presence. Consumers can buy apps, streaming subscriptions, online courses, cloud tools, digital advertising, software and professional services from foreign providers.

KRA states that non-resident persons making supplies in Kenya over the internet, electronic networks or digital marketplaces are required to register for VAT whether or not their taxable supplies meet the annual KES 5 million threshold, and that a simplified registration, filing and payment system has been developed for suppliers. :contentReference[oaicite:13]{index=13}

This reflects a broader global challenge: tax systems built for physical trade must now capture digital consumption. The OECD notes that cross-border online shopping has increased interaction among national VAT systems. :contentReference[oaicite:14]{index=14}

For consumers, this can mean VAT appears on digital subscriptions or online purchases. For businesses, it means digital procurement and digital sales must be reviewed for VAT treatment. A company using foreign software or selling digital services to customers in different countries may face more complex compliance than a traditional local business.

Withholding VAT

Some VAT systems use withholding mechanisms where appointed agents withhold part of VAT from payments to suppliers and remit it to the tax authority. This is designed to improve compliance and reduce revenue leakage.

In Kenya, KRA states that withholding VAT is charged at 2 percent of the value of taxable supplies, with no VAT withheld on exempt goods, exempt services and zero-rated supplies. KRA also notes that a taxpayer whose VAT has been withheld is still required to submit an online VAT return and account for the VAT balance. :contentReference[oaicite:15]{index=15}

For suppliers, withholding VAT affects cash flow and reconciliation. The customer may withhold part of the VAT and remit it directly, while the supplier must account for it properly in the return. If records are poor, the supplier may struggle to match withheld VAT credits with sales.

Withholding VAT also shows why VAT compliance is not only about calculating a rate. It is about understanding the customer, transaction type and tax mechanism involved.

VAT and Small Businesses

VAT can be especially difficult for small businesses because it adds administrative complexity at the same time the business is trying to grow.

Before registration, a small business may quote simple prices, keep basic records and focus mainly on sales. After registration, it must charge VAT correctly, issue compliant invoices, track input tax, file returns, maintain records and manage tax payments. The business may need accounting software, professional support and stronger internal controls.

Registration can also affect competitiveness. If a business sells mainly to consumers, adding VAT may make prices look higher unless the business absorbs part of the tax, which reduces margins. If the business sells mainly to VAT-registered companies, VAT may be less of a pricing barrier because customers may claim input tax.

A small business approaching the VAT threshold should plan early. It should review pricing, contracts, accounting systems, customer mix, supplier invoices and cash-flow reserves. It should decide whether quoted prices will be VAT-inclusive or VAT-exclusive. It should educate staff handling invoices and receipts.

The worst time to learn VAT is after penalties, client disputes or cash-flow pressure have already appeared.

VAT and Profit: Why They Are Not the Same

VAT collected is not profit.

This sounds obvious, but it is one of the most common mistakes in small business finance. A business receives money from customers and sees a healthy bank balance. The owner spends from that balance on salaries, rent, stock, personal drawings or expansion. Later, the VAT deadline arrives, and the business does not have enough cash to remit tax.

The problem is mental accounting. The VAT portion of receipts should be treated as money held temporarily. It may pass through the business bank account, but it does not belong to the business in the same way net sales revenue does.

A disciplined business can separate VAT cash physically or mentally. Some businesses maintain a tax reserve account. Others transfer estimated VAT weekly. Others use accounting dashboards to track VAT payable. The method matters less than the discipline.

Profit is what remains after costs, taxes and obligations. VAT collected is a liability until properly accounted for.

VAT and Consumers: Why Prices Feel Higher

Consumers experience VAT through prices. A consumer may not care whether a business is claiming input tax or filing monthly returns. They care about the final amount paid.

VAT can make goods and services feel more expensive because it is embedded in consumption. When household budgets are tight, VAT on everyday spending becomes highly visible. Even where essential goods are zero-rated or exempt, VAT may still affect the cost structure of businesses supplying those goods if input tax cannot be recovered in full.

This is why VAT policy can be politically sensitive. A broad VAT base raises revenue efficiently, but it may affect lower-income households more heavily as a share of income. Governments often try to balance revenue needs with social protection through exemptions, zero-rating or targeted relief. The design is never simple because exemptions can reduce revenue, complicate compliance and create classification disputes.

For consumers, the practical lesson is that taxes are part of the cost of living. Understanding VAT helps explain why final prices differ from pre-tax prices and why tax policy changes can affect household budgets.

VAT and Business-to-Business Transactions

In business-to-business transactions, VAT often functions differently from consumer sales.

If both buyer and seller are VAT-registered and the purchase is used for taxable business activity, the buyer may claim input tax. This means VAT may not be a final cost for the buyer, though it still affects cash flow. The buyer pays VAT to the supplier and recovers it through the return mechanism, assuming all requirements are met.

This is why VAT-registered corporate clients often insist on proper tax invoices. Without a valid invoice, they may lose the ability to claim input tax. A supplier who cannot issue compliant invoices may appear less attractive to corporate buyers.

For a small business selling to larger companies, VAT registration may therefore be commercially useful once the business reaches scale. But the business must comply properly. Corporate customers may reject invoices with missing PINs, incorrect VAT amounts or non-compliant documentation.

VAT compliance can become part of market access.

VAT and Exempt Businesses

Businesses making exempt supplies face a different challenge. They may not charge VAT to customers, but they may also be unable to claim input tax on related purchases. This can increase costs.

For example, if an exempt business buys taxable professional services, equipment, rent, software or supplies, the VAT paid may become part of its cost base. Since the business cannot recover the VAT, it may need to reflect that cost in pricing. This can make exempt businesses sensitive to VAT on inputs even though they do not charge VAT on outputs.

Businesses with mixed supplies, meaning some taxable and some exempt, may face more complex apportionment rules. They may only claim input tax related to taxable supplies or may need to allocate input tax according to prescribed methods. This is an area where professional advice is often necessary.

Exemption can help consumers by removing VAT from certain final supplies, but it can complicate business cost structures.

VAT Fraud and Compliance Controls

VAT systems are vulnerable to fraud because input tax credits create opportunities for false claims, missing trader schemes, fake invoices and circular transactions. Tax authorities therefore use compliance controls, electronic invoicing, audits and special monitoring systems.

KRA describes a VAT Special Table mechanism in iTax intended to enhance compliance, including categories such as nil filers, non-filers and missing traders. KRA states that taxpayers on the Special Table may be restricted from filing VAT returns and that traders cannot claim input tax from taxpayers on the table. :contentReference[oaicite:16]{index=16}

For honest businesses, this means supplier due diligence matters. A business may lose input tax claims if it deals with non-compliant or suspicious suppliers. It is not enough to receive an invoice. The supplier’s compliance status may affect the buyer’s tax position.

Compliance should therefore include careful supplier onboarding, invoice validation, recordkeeping and regular reconciliation. VAT fraud controls can affect even businesses that did not intend to participate in wrongdoing.

VAT Planning Is Not VAT Evasion

Businesses are allowed to plan their affairs within the law. VAT planning may include understanding whether supplies are taxable, zero-rated or exempt; structuring contracts clearly; claiming valid input tax; maintaining proper documentation; timing purchases and sales carefully; using compliant systems; and seeking refunds where allowed.

VAT evasion is different. It includes deliberately failing to register, suppressing sales, issuing fake invoices, claiming false input tax, misclassifying supplies, underreporting output tax or creating artificial transactions to avoid tax.

The difference is ethics and legality. Good VAT planning improves compliance and protects cash flow. VAT evasion creates penalties, interest, legal exposure and reputational damage.

A serious business should not view tax compliance as a burden separate from financial management. VAT discipline is part of operating professionally.

How VAT Affects Investment Decisions

VAT can affect investment decisions, especially for business owners and property investors.

A business buying machinery, vehicles, equipment, software or construction services must consider VAT in the total cost. If input tax is recoverable, the VAT may be a temporary cash-flow cost. If it is not recoverable, it becomes part of the investment cost. This affects return calculations.

A property developer or landlord must understand whether the relevant supplies are taxable or exempt and whether input tax can be claimed. A manufacturer investing in equipment must consider import VAT, customs procedures and input tax timing. A professional firm investing in technology must consider VAT on local and imported services.

VAT also affects mergers, acquisitions and business sales. Buyers may need to assess VAT liabilities, registration status, unpaid tax, input tax claims, invoicing compliance and potential audit exposure. A company with poor VAT records may carry hidden liabilities.

Investors should therefore treat VAT as part of due diligence. Tax compliance affects business value.

How to Build a Strong VAT System

A business can manage VAT better by building a system rather than relying on memory.

The first step is classification. Know which sales are standard-rated, zero-rated, exempt or outside scope. Know which purchases support taxable supplies and which do not.

The second step is invoicing. Use compliant invoicing tools, issue tax invoices promptly, include correct customer and supplier details, and ensure VAT is calculated correctly.

The third step is recordkeeping. Store sales invoices, purchase invoices, import documents, credit notes, debit notes, payment records, contracts and tax returns in an organized way.

The fourth step is reconciliation. Compare sales records, bank receipts, invoices, accounting system reports and VAT returns. Differences should be investigated before filing.

The fifth step is cash reservation. Set aside VAT collected so payment deadlines do not create stress.

The sixth step is review. VAT rules can change. Businesses should periodically review rates, thresholds, exemptions, digital services rules and invoicing requirements with qualified advisers.

The seventh step is responsibility. Someone in the business must own VAT compliance. If everyone assumes someone else is handling it, mistakes multiply.

Common VAT Mistakes

The first mistake is failing to register on time. A business crossing the threshold without registering may create backdated liabilities.

The second mistake is quoting prices without saying whether VAT is included or excluded. This can reduce margins or create client disputes.

The third mistake is treating VAT collected as spendable income. This creates cash-flow pressure when payment is due.

The fourth mistake is losing valid tax invoices. Without documentation, input tax claims may be denied.

The fifth mistake is claiming input tax on purchases not used for taxable supplies or outside the allowed time limits.

The sixth mistake is applying the wrong VAT treatment to zero-rated or exempt supplies.

The seventh mistake is ignoring imported services and digital purchases from non-resident suppliers.

The eighth mistake is filing late or filing nil returns when taxable activity occurred.

The ninth mistake is failing to reconcile withholding VAT credits.

The tenth mistake is assuming an accountant can fix everything after records have been neglected for months.

VAT for Freelancers and Consultants

Freelancers and consultants often enter VAT gradually. At first, they may operate below the registration threshold. As income grows, they may begin serving larger clients, billing more regularly and approaching mandatory registration.

The transition requires planning. A freelancer who suddenly becomes VAT-registered may need to update proposals, contracts, invoices and pricing. Clients should be informed whether future invoices will include VAT. The freelancer should track business expenses and preserve tax invoices for software, equipment, professional services, internet, office costs and other allowable inputs where applicable.

Freelancers selling to corporate clients may find that VAT registration improves credibility, especially if clients prefer dealing with formal suppliers. But freelancers selling to consumers may find VAT affects price sensitivity.

The key is not to wait until registration becomes urgent. A growing freelancer should understand VAT before the threshold is crossed.

VAT for Retailers

Retailers handle VAT differently because they sell frequently, often to final consumers. Their prices are usually VAT-inclusive, and transaction volumes can be high.

A retailer must ensure point-of-sale systems, inventory systems and electronic tax invoicing tools calculate VAT correctly. Different goods may have different VAT treatments. Some may be standard-rated, some zero-rated, some exempt. Misclassification across thousands of transactions can create significant errors.

Retailers also need strong purchase records because input tax claims may be substantial. Supplier invoices, inventory purchases, returns, discounts and credit notes must be captured accurately.

Retail VAT compliance is operational. It depends on systems, staff training and daily discipline.

VAT for Importers

Importers must think about VAT before goods arrive.

The landed cost of imported goods can include purchase price, freight, insurance, customs duty, import declaration fees, clearing costs, port charges and VAT. If the importer is VAT-registered and the goods support taxable supplies, import VAT may be recoverable. But it still affects cash flow because money may be paid before the goods are sold.

Importers should price goods based on full landed cost, not supplier price alone. Underestimating VAT and related charges can make a product appear profitable when it is not.

Documentation is also critical. Import entries, customs documents, supplier invoices, freight documents and payment records support accounting and tax claims. Poor import records can create disputes and lost input tax.

VAT and Professional Advice

VAT can appear simple in basic examples, but real business situations become complex quickly. Mixed supplies, imported services, digital marketplaces, property transactions, partial exemption, cross-border trade, bad debts, credit notes, group structures and industry-specific rules may require professional advice.

A qualified tax adviser or accountant can help classify supplies, review contracts, set up systems, prepare returns, manage audits and avoid costly errors. Professional advice is especially important before major transactions, not after problems appear.

Business owners should not delegate understanding completely. Even with an adviser, the owner should know the basic VAT logic. They should understand what is being charged, what is being claimed, when returns are due and how VAT affects cash flow.

Advice works best when the business owner remains engaged.

Final Thoughts

Value Added Tax is more than a tax line on a receipt. It is a system that connects consumers, businesses and government through the ordinary act of buying and selling.

Consumers usually bear VAT through prices. Businesses collect it, account for it and remit it. Governments rely on it because consumption is broad and recurring. The system works through the difference between output tax charged on sales and input tax paid on qualifying purchases.

For households, VAT affects the cost of living. For businesses, it affects pricing, cash flow, documentation, supplier relationships, contracts, imports, digital purchases and compliance risk. For investors, it can affect margins, asset costs and business valuation.

The most important lesson is that VAT must be managed deliberately. A business should know when registration is required, whether prices are VAT-inclusive or exclusive, which supplies are taxable, which purchases support input tax claims, when returns are due and how much cash must be reserved for payment.

VAT collected is not profit. VAT paid is not always recoverable. VAT exemption is not the same as zero-rating. A valid tax invoice is not a formality. A missed deadline is not harmless. These distinctions determine whether VAT becomes a manageable system or a recurring financial problem.

Financial education often focuses on earning, saving and investing. But taxes shape all three. A person who understands VAT understands prices more clearly. A business owner who understands VAT protects margins and cash flow. An investor who understands VAT sees business economics more accurately.

VAT may be invisible to many consumers, but it is never irrelevant.